During the last 7 years, the percentage of Poles who save on a regular basis has grown more than twofold - such is the conclusion coming from the data of The Citi Handlowy Leopold Kronenberg Foundation. Although in terms of value of collected funds there is still a lot to do as compared with other European countries, as many as 67 percent of Poles think that it pays off to save.

It has been known for a long time that success in saving may only be secured by its regularity. This year eighth edition of the research of The Citi Handlowy Leopold Kronenberg Foundation entitled "Poles' Attitudes Towards Saving" proved that as many as 59 percent of Poles save money having in mind their future. It is not a bad result, however taking into account the amounts we put off at banks or on policies, we are still lagging far behind the German, French or British and even behind the other central Europe countries, such as Czech Republic, Hungary or Croatia. A statistical Pole keeps EUR 6 thousand on their account. To compare, the German has EUR 44 thousand, the French - EUR 50 thousand and the British - EUR 86 thousand, according to 2015 Allianz Global Wealth Report.

Continuous reductions of interest rates of bank term deposits and other deposits theoretically should discourage from regular saving. In years 2013 to 2015, the Monetary Policy Council has cut interest rates eight times. Such cuts has been followed by reductions in bank deposit interest rates - for annual PLN 10 thousand deposits it does not exceed the average level of 1.60 percent. The Monetary Policy Council has not changed the interest rates, which means that loans will still remain at a record low level.

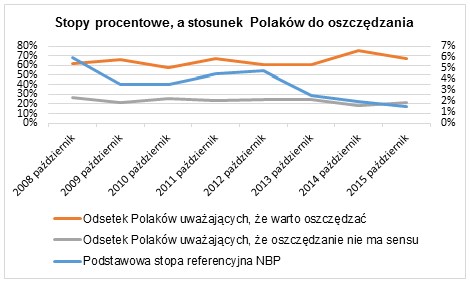

Nevertheless, it turns out that within the last 7 years the percentage of Poles who think that it is worth saving has increased from 62 to 67 percent, and the size of the group considering saving senseless fell by 6 percentage points. Importantly, the number of people who manage to save funds for the future on a regular basis has grown significantly - in 2008 it was 7 percent of Poles, today it is 16 percent. It is also worth noting that our society has ever greater amounts at its disposal - the data gathered by the Central Statistical Office show that our real income has grown by more than 10 percent in the last 7 years.

October 2008, October 2009, October 2010, October 2011, October 2012, October 2013, October 2014, October 2015

Percentage of Poles who believe that it is worth saving

Percentage of Poles who believe that saving is senseless

Basic reference rate of the National Bank of Poland

Therefore, there are all indications that Poles' knowledge about finance and the awareness that it is worth saving having in mind the future, irrespective of the economic environment, are growing. Experts convince that interest on deposit is not the only prerequisite for effective saving.

The profit resulting from regular saving of even small amounts comes from the power of compound interest, explains Krzysztof Kaczmar, President of the Management Board of The Citi Handlowy Leopold Kronenberg Foundation. We shall be aware that keeping money on a bank term deposit or a different deposit gives us in each consecutive year an interest not only on principal but also on the profit credited in the previous settlement period. This effect of snowball makes regular and long term saving pay off even if interest rate on the account is low.

We should also be aware that saving is favored by record low inflation rate prevailing in Poland. November 2015 was the seventeenth month in a row witnessing falls in prices. Also the purchasing power of saved money is growing while the funds which are frozen on deposits do not lose their value with time. What is more, with our monthly remuneration we may buy more than for example two years ago. It is worthwhile taking advantage of this situation and putting off financial surpluses instead of spending them, having in mind more important future goals.